For any business in any industry—from an early-stage company to a mature organization—cash flow is imperative to the decision-making process. With liquid capital, you can better capitalize on opportunities and make decisions that would otherwise leave you at the behest of investors, donors, grants, and the like. Since all aspects in business depend on financial fluidity, a dynamic forecast and a well-built cash flow model are essential to drive sustainable success and improve agility, irrespective of where you are in your business life cycle.

Effective cash flow modeling (as opposed to stagnant reports):

- Gives you the ability to model scenarios based on data

- Helps you quickly identify profitable areas and cash pitfalls

- Allows you to recognize trends across customer behaviors

- Informs more strategic decision-making and measured risk-taking

Ultimately, predictive modeling and informative cash flow insights can revolutionize the way your business spends precious dollars.

For the Early Stage Company | What is Cash Flow and Burn?

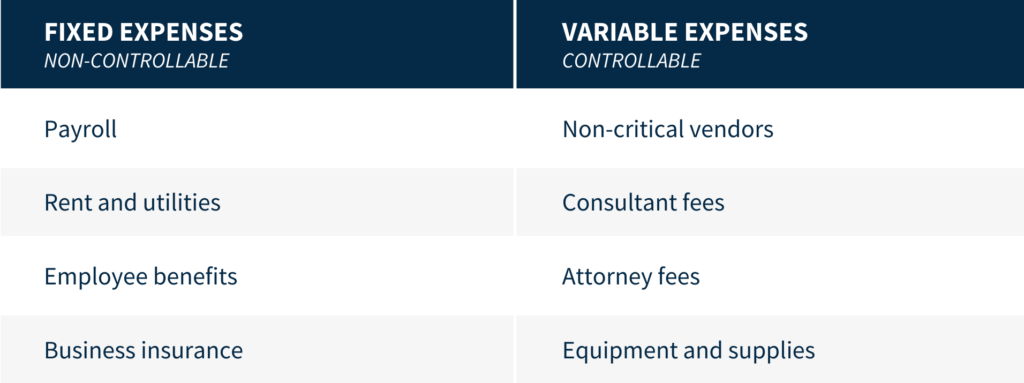

Cash flow can be defined as the money from customer payments, grants, investor capital, sales (of products or assets like equipment), and tax refunds. Cash is then spent on fixed or variable expenses like:

When outgoing money is more than incoming money, we call this your burn rate. Tied to this is your runway—the amount of time an entity has before it depletes its liquid cash. For example, if a company has $100,000 in the bank and spends $20,000 each month (the burn rate), it has a runway of five months.

As pre-revenue businesses evaluate spending, it is important to have clear insights about major expense areas and keep updated records. This is especially true for entities that are dependent upon investor capital. Investors are always looking for companies that are pre-revenue or cash flow negative to extend their runway and slow their burn rate. To learn more, watch our Managing Cash Flow Through a Crisis webinar recording.

For Mature Organizations and Early Stage Companies | What Are Tips for Improving Cash Flow?

Long-term financial management is the cornerstone of any profitable entity. Having a competent, intuitive financial leader or CFO (whether in-house or an outsourced partner) with the expertise to build accurate models and projections is critical to establishing and maintaining financial security.

An accurate, dynamic, timely, and dependable cash flow model is imperative to slow burn and assess risk and opportunity. It allows those scrutinizing your financials to identify predictable and stable data points first, then comb through historical data for unusual activity. This will enable your organization to reassess where it can make changes that could decelerate or accelerate positive cash flow. With a proper cash flow model, you can analyze both fixed and variable expenses (including other factors) like:

- Reviewing people and payroll practices

Understand where you can save time, money, and resources while still achieving the same or better outcomes. Ask yourself: How can we more effectively manage overtime? Where can we outsource for improved efficiency at a lesser cost? - Rethink fixed expenses, like rent

Regularly review your lease terms and propose solutions based on company activity and needs, especially with remote work on the rise. Ask yourself: Do we have an opportunity to downsize, sublet, or eliminate office space? This is just one example. The right CFO can help you define and manage all fixed expenses to benefit the business. - Create customer incentives

Explore opportunities to adjust payment terms to the benefit of customers and your company. Ask yourself: Can we experiment with things like discounts for early or pre-payments or require a portion of a payment upfront? - Improve protocols

Implement and/or optimize internal spending protocols that align with budgets and cash flow requirements to streamline activity and define best practices. Ask yourself: What changes can we make across the organization to save money and increase our margins? - Leverage your bank

Explore loan options through the Small Business Association (SBA) and even inquire about reducing fees associated with your account(s). Ask yourself: In what areas do we see an opportunity to reduce monthly spend on extraneous expenses? - Consider financing options

Payment terms and leases may be negotiable with vendors and services providers. Find opportunities to cut spending where possible and reduce overhead where possible. Ask yourself: If this expense isn’t directly attributed to creating our product or service, how can we reduce or eliminate it? - Utilize technologies

Financial leaders may want cloud-based technologies to automate processes, streamline functionalities, mitigate risks associated with human error, and allow for accurate and timely reporting. Ask yourself: What systems or applications are no longer serving our requirements and risk negatively impacting our business operations?

Effective cash flow management keeps your business operating efficiently and positions you to take advantage of growth opportunities. Finding creative ways to build better margins keeps your company resilient, agile, and prepared even in unanticipated circumstances.

Ready to Elevate Your Expense Management Practices?

By getting creative with expense management/cash flow modeling and leveraging the right partner or in-house personnel to analyze budgets and identify ways to “trim the fat,” your business can increase its margins and gain more financial flexibility to make informed business decisions. For additional insight or to get started, contact our Accounting Solutions team.