Certain small business taxpayers with average aggregated gross receipts of $26 million or less for 2019 and 2020 (adjusted annually for inflation) may be exempt from the Sec. 163(j) limitation on business interest expense deductions. The IRS has released FAQs regarding the aggregation rules.

Background

Generally, small business taxpayers with average aggregated gross receipts of $26 million or less for 2019 and 2020 may be exempt from the Sec. 163(j) limitation on business interest expense deductions. This limitation was created by the Tax Cuts and Jobs Act of 2017 and later adjusted by the CARES Act in 2020 (see our blog here).

The gross receipts are calculated as the average over the past three taxable years, and the $26 million threshold is adjusted annually for inflation. To determine whether a taxpayer meets the gross receipts test, you must apply the aggregation rules under Section 448(c)(2). While this code section generally only applies to corporations and partnerships with a C corporation partner, the IRS has specifically stated that it applies to all taxpayers for the purposes of determining gross receipts under Sec. 163(j). In the FAQs posted, the IRS addressed the aggregation rules into three parts.

Part 1: All Entities Considered for Aggregation are Corporations

When all potential entities considered for aggregation are corporations, taxpayers may need to aggregate gross receipts as a parent-subsidiary controlled group, a brother-sister controlled group, or a combined group of corporations.

- A parent-subsidiary controlled group is one in which there is a common parent corporation that owns more than 50% of the combined voting power or share value of at least one of the other corporations. The group will also include any corporation owned more than 50% by any corporation that is a member of the group.

Example: P Corporation owns 80% of T Corporation and T Corporation owns 80% of X Corporation. In this scenario, this is a parent-subsidiary controlled group in which P is the parent and T and X are the subsidiaries.

- A brother-sister controlled group is one in which five or fewer individuals, estates or trusts meet both the 80% ownership requirement and the identical ownership requirement. This means that five or fewer persons own at least 80% of the combined voting power or share value of each corporation and the same persons, only taking ownerships into account to the extent it is identical with respect to each corporation, own more than 50% of each corporation.

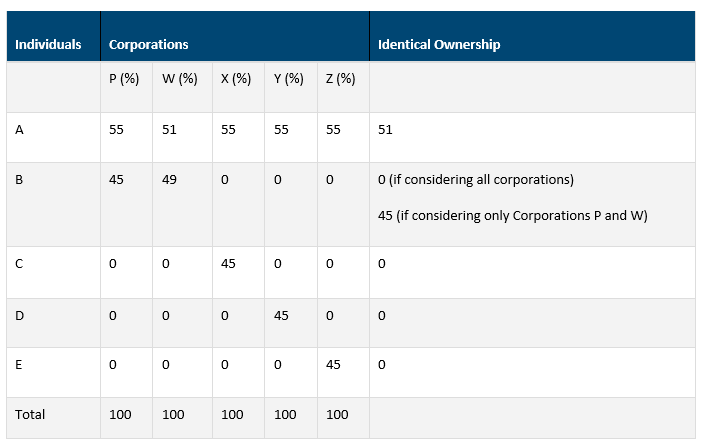

Example:

Corporations P, W, X, Y, and Z are not members of a brother-sister controlled group because the 80% ownership requirement is not met. Individual A is the only common owner of all five corporations, so only its ownership % (either 55% or 51% in this case) is counted towards the 80% requirement. However, Corporations P and W are members of a brother-sister controlled group.

- A combined group of corporations is three or more corporations in which all are members of either a parent-subsidiary controlled group or a brother-sister controlled group and at least one of the corporations is both the common parent of a parent-subsidiary controlled group and a member of a brother-sister controlled group.

Ownership used to determine parent-subsidiary controlled groups and brother-sister controlled groups includes stock owned directly and owned constructively. Constructive ownership includes any person who has the option to acquire stock of a corporation and any person who owns 5% or more of a partnership, estate or trust that owns stock of a corporation.

Brother-sister controlled groups have additional constructive ownership rules. Any person who owns 5% or more of a corporation (A) that in turn owns stock in another corporation (B) is deemed to own a proportionate share of the stock of Corporation B. Additionally, a person is generally considered to own stock of a corporation that is owned by his or her spouse and children under 21. If a person owns more than 50% of a corporation, that person is deemed to also own any stock of the corporation owned by that person’s parents, grandparents, grandchildren, and children 21 and over.

Part 2: Entities Considered for Aggregation are Partnerships, Trusts, Estates, Corporations or Sole Proprietorships

Similar to when all entities considered for aggregation are corporations, taxpayers that are partnerships, trusts, estates, corporations or sole proprietorships may be required to aggregate gross receipts as a parent-subsidiary group, a brother-sister group, or a combined group under common control.

The parent-subsidiary group rules are generally the same as those listed for corporations. One of the entities must be a common parent and it must own 50% or more of a corporation, partnership, trust, or estate. For a sole proprietorship, the sole proprietor must be the individual.

The brother-sister group definition wording differs slightly from the corporation 80% ownership requirement and the identical ownership requirement. Instead, a brother-sister group is one in which five or fewer persons meet the controlling interest requirement and the effective control requirement. While the wording is different, in concept the controlling interest requirement and the effective control requirement are applied in the same manner as the 80% ownership requirement and the identical ownership requirement.

Part 3: Entities Considered for Aggregation are Affiliated Service Groups

Affiliated service groups do not have sufficient common ownership or control to be considered a controlled group but may still require the gross receipts to be aggregated. Section 414(m)(2) outlines two types of affiliated service groups that require a combination of common ownership and performance of services among the organizations. Section 414(m)(5) outlines a third type of affiliated service group which does not require common ownership but instead aggregates employers based on the performance of management services provided by one organization for another.

The affiliated service groups that require common ownership consist of a service organization and either an “A organization” or a “B organization.” An “A organization” is a service organization that is an owner of and either performs services for or with the first service organization. A “B organization” is an other organization whose business involves a significant performance of services (for either the first service organization or “A organization”) of a type historically performed in the service field by employees and is owned at least 10% by highly compensated employees of the first service organization or an “A organization.”

The affiliated service group that does not require common ownership is commonly referred to as a management affiliated service group. This group consists of an organization whose principal business is performing management functions and the organization who receives these management services.

Please let your SC&H team know if you have questions, and keep our Coronavirus Resource Center bookmarked for updates on new guidance and legislative relief we expect Congress to provide in the near future.