Authored by Frank Paolantonio | Senior Associate

For many business owners, the question isn’t if you’ll exit, but how.

As retirement nears or your priorities shift toward succession, you may find yourself weighing the same three paths: selling to a strategic buyer, selling to a private equity (PE) firm, or transitioning ownership through an Employee Stock Ownership Plan (ESOP).

While strategic buyers may offer higher headline purchase prices, what truly matters is what you keep after your taxes. On that front, ESOPs can be surprisingly competitive, and in some cases, deliver even better after-tax results than a traditional third-party sale.

Financial results, however, are only part of the story. For many founders and shareholders, an ESOP also provides a way to preserve the company’s legacy, reward employees, and maintain continuity for customers and communities while achieving meaningful liquidity and tax advantages.

As you evaluate your exit options, understanding how ESOPs compare to PE and strategic sales—both from a financial and strategic perspective—can help you make a more confident and informed decision about what’s right for you and your company’s future.

In this article, you’ll learn:

- How ESOPs can produce competitive or superior after-tax proceeds for selling shareholders

- The unique tax advantages available to C corporation and S corporation owners

- How ESOP structures can support legacy preservation and employee engagement

- Key considerations to help determine whether an ESOP aligns with your personal and financial goals

For business owners seeking liquidity, tax efficiency, and a lasting impact, an ESOP isn’t just an alternative — it may be the most strategic path forward.

Understanding ESOP Valuation and Net Proceeds

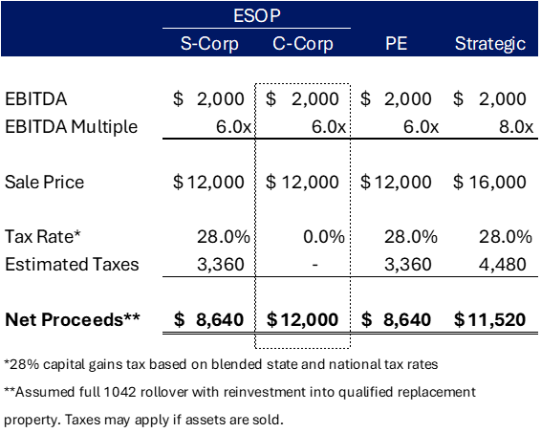

It’s easy to focus on the top-line purchase price, but net proceeds after taxes ultimately determine the true value. While strategic buyers or PE firms may offer higher valuations, the net outcome of an ESOP sale often tells a different story.

ESOPs offer unique tax advantages that can significantly boost net proceeds. Under Section 1042 of the Internal Revenue Code (IRC), owners of C corporations who sell at least 30% of their shares to an ESOP can defer capital gains taxes indefinitely by reinvesting in Qualified Replacement Property (QRP). By comparison, a sale to a private equity or strategic buyer typically triggers immediate capital gains taxes, which can reduce take-home proceeds by 20-30 percent or more.

To illustrate this difference, the example below compares net proceeds between the various sale options:

The difference can have a meaningful impact. Relative to PE sales with a similar multiple or even a strategic buyer at a higher multiple, the ESOP can still match or beat the seller’s take-home proceeds when selling as a C corp.

ESOPs also offer long-term benefits for both owners and the company:

- For C corporation sellers: The 1042 rollover provides a powerful way to preserve and grow wealth while deferring taxes.

- For S corporation ESOPs: Once the ESOP owns 100 percent of the company, it becomes federally income tax-exempt and, in many states, also free from state corporate taxes. The result is stronger cash flow and enhanced company value over time.

If you’re focused on preserving legacy, employee impact, and tax efficiency, the combination of competitive valuations and favorable after-tax outcomes can be a true game-changer, making an ESOP an especially attractive exit strategy.

Tax Deferral Strategies for Owners in an ESOP C Corp Sale

When selling to an ESOP, C Corp owners enjoy a powerful tax planning opportunity under IRC Section 1042. Under this provision, owners who sell at least 30 percent of their share to an ESOP can defer capital gains taxes indefinitely by reinvesting the proceeds into Qualified Replacement Property (QRP).

This approach allows owners to potentially preserve significant wealth. Common QRP options include:

- Publicly traded U.S. corporate stocks (excluding mutual funds and foreign companies)

- Diversified portfolios of eligible equities managed by 1042 specialists

While the benefits are substantial, a 1042 rollover does come with certain limitations. One of the primary downsides is that sellers cannot access the sale proceeds for personal spending (i.e. buying a new boat or beach house may not be immediately attainable). Liquidating or directly accessing the principal would trigger the deferred capital gains and eliminate the advantage of the rollover. For many owners, this restriction may not align with their retirement lifestyle goals.

However, with careful planning, experienced 1042 advisors can help design custom QRP strategies that balance compliance, diversification, and liquidity with lifestyle needs. Considering your goals, advisors often build diversified QRP portfolios that generate steady interest and dividend income that provides ongoing cash flow for the seller.

Additionally, advisors can use structured lending strategies that allow owners to borrow against their QRP holdings. This approach provides access to liquidity without triggering a taxable event.

When executed thoughtfully, the 1042 rollover can serve as a flexible wealth preservation and tax-deferral strategy, though the process can be complex and often requires specialized guidance.

It’s important to note, however, that the primary benefit of the 1042 rollover applies only to the selling shareholder, not the company itself. The corporate tax benefit of a C Corp ESOP is the deductibility of principal and interest, subject to payroll-based limitations, on the stock acquisition related debt. In contrast, an S Corp that transitions to full ESOP ownership enjoys ongoing federal tax exemption, which can have a dramatic impact on company cash flow, growth, and long-term value.

Tax Exemption Advantages for Companies in an ESOP S Corp Sale

In an ESOP sale involving an S Corp, owners and shareholders generally must recognize capital gains at the time of the transaction. However, recent legislation under Secure Act 2.0 allows for limited tax deferral for S Corp shareholders beginning in 2028.

The most compelling advantage of an S corporation ESOP is the company’s exemption from federal income tax once the ESOP owns 100 percent of the shares. In many states, the business also qualifies for an exemption from state corporate income taxes.

C corporations do not receive this same ongoing exemption and must continue to pay corporate income taxes, albeit with the benefit of enhanced deductibility for acquisition related principal and interest payments. However, for C Corps that wish to capture these tax benefits, there is an option. After completing the ESOP transaction, the company may elect S Corp status, provided it has been a C Corp for at least five taxable periods. The IRS maintains strict rules around these elections and does not allow frequent changes, but for qualifying businesses; this transition can unlock additional tax efficiencies and improve cash flow over time.

What’s Next? Explore Whether an ESOP Sale is Right for Your Business

If you’re considering an exit and want to understand whether an ESOP could be the right path for your company, a feasibility study is the best place to start. This analysis provides a detailed look at your company’s financial performance, valuation range, and transaction options to determine how an ESOP could align with your ownership goals.

During a feasibility study, ESOP specialists help you:

- Assess your company’s valuation and potential sale structure

- Evaluate transaction financing options and the ability to support ESOP debt

- Estimate after-tax proceeds for C Corp and S Corp scenarios in coordination with your tax advisor

- Understand the impact on employees, leadership, and corporate governance post-transaction

- Explore management incentive plans commonly used in ESOPs to further motivate and retain key employees

The process provides clarity around how an ESOP would perform relative to other exit strategies, so you can make a confident and informed decision about your next steps.

If you’re ready to explore whether an ESOP could be the right fit for your business, the SC&H ESOP team can guide you through the feasibility study and help you evaluate your options. Our specialists bring deep experience in valuation, transaction structuring, and tax planning, providing the insight you need to make an informed decision with confidence.

The ESOP Advantage for a Strategic and Rewarding Business Exit

An ESOP offers more than a sale; it’s a way to achieve liquidity, tax efficiency, and legacy preservation while rewarding the people who helped build your company’s success. For many owners, the ability to structure a transaction that provides financial security, sustains company culture, and supports employees is what makes an ESOP truly unique.

Whether through tax deferral and wealth preservation in a C Corp ESOP or tax exemption and stronger cash flow in an S Corp ESOP, this structure can deliver powerful outcomes for both shareholders and companies.

However, an ESOP isn’t right for every situation. It requires careful analysis, thoughtful planning, and guidance from experienced advisors who understand both the technical and cultural considerations of ownership transition.

For many business owners, an ESOP represents more than an exit—it’s a strategic way to protect what you’ve built, reward the people who helped create it, and ensure the company’s success for generations to come.