Client Login

SC&H

March 30, 2026

What Multi-State Hiring Really Means for Payroll Compliance

March 25, 2026

How to Navigate the Microsoft SSPA Assessment: A Step-by-Step Guide for Suppliers

March 16, 2026

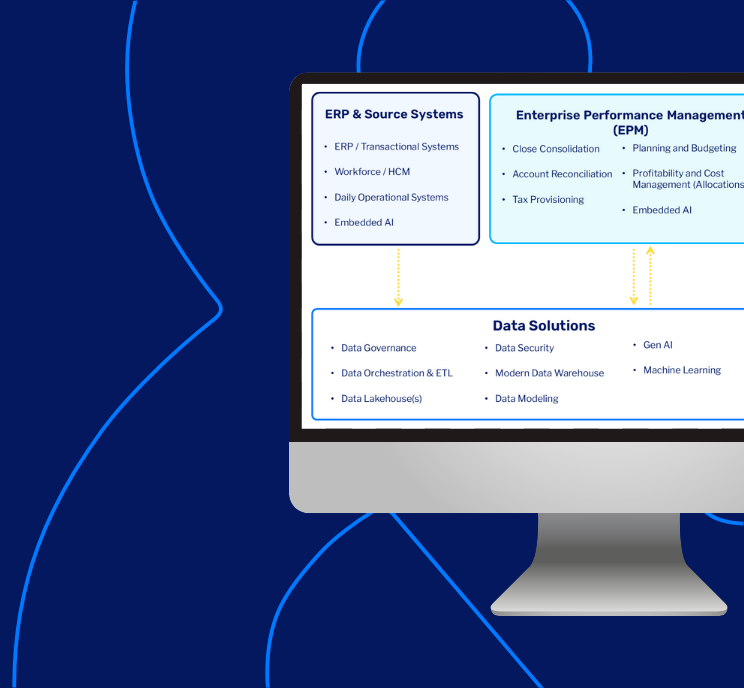

The Challenges of Hyperscale Data Center Construction: Built for Speed, Exposed to Risk

February 26, 2026

Healthcare & Life Sciences: Data & Technology Trends for 2026

February 20, 2026

A Smarter Approach to the College Search

February 3, 2026

Business Continuity Planning: How to Get Ahead of the Next AWS Outage

January 29, 2026

A Guide to Budgeting & Forecasting for SMBs (With a FREE Template!)

December 19, 2025

Refinancing in a Volatile Private-Credit Market: What Borrowers and Lenders Need to Know

The CFO’s Guide to Building an IT Budget: Best Practices, Examples, + How Much to Spend

December 15, 2025

How to Implement Oracle IPM: A 90-Day Pilot for AI Forecasting

December 8, 2025

2025 Year-End Tax Planning Seminar

November 25, 2025

Building a Modern, Connected Flavor Manufacturing Operation

November 17, 2025

Words Matter: Protect Your CapEx Investment Before You Build

November 5, 2025

Incremental IT Modernization: How to Achieve Big Results Without a Big Bang Budget

Selling Your Business: The Hidden Value of an ESOP Exit

October 6, 2025

Top 5 Reasons for Accounts Payable Overpayments (and How to Prevent Them)

September 25, 2025

Unifying Hilton’s Global Financial Operations with Oracle EPM

September 24, 2025

Nonprofit Scenario Planning Guide + Template: How to Navigate Funding Cuts in 2025

September 17, 2025

Redefining Finance: How Forward-Looking CFOs Are Building Future-Ready Teams and Tech Stacks

September 5, 2025

Critical Event Payment Readiness: Managing Financial Transactions Amid Chaos

August 18, 2025

Stay in Control: Spot the Early Signs of Contract Risk in Fixed-Price Construction Projects

August 6, 2025

From Default to Ownership: Inside Private Credit Lender Workouts

August 4, 2025

Individual Tax Planning Strategies and Tips for the One Big Beautiful Bill

August 1, 2025

How 3 Depreciation Changes Are Promoting Business Investment

A collection of insights about our capabilities, solutions, people, and client successes.

Enter Your Email Address

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.