Authored By Angelo Romano, CFP® | Wealth Advisor, SC&H Wealth

If you’ve already opened a 529 college savings plan (or you’re considering opening one), you’re already on the right track to securing your child’s future education. By proactively saving money, you can avoid expensive educational loans that can be three times more costly than saving for college.

However, there are a few valuable ways you can extract even greater value from your investment. In this article, we share our top strategies to maximize the benefits of your 529 plan and supercharge your savings.

1. Start Saving Early!

Time makes all the difference in an investment fund. The earlier you start, the more your money compounds.

For example: If you start saving $100 a month when your child is born and your 529 investments earn a 5% return, you could have an account balance of 34,920 by age 18 to help pay for their education expenses. Conversely, waiting until your child is 9 years old to start saving will only provide $13,604 towards college expenses. In this example, doubling the investment timeframe results in an ending 529 account value that is more than 2.5 times greater.

2. Prioritize Your 529 College Savings Plan Contributions According to Your Financial Situation.

These funds should not be prioritized over retirement savings or an emergency fund. Maintaining your retirement’s planned funding levels takes precedence, even if this means underfunding your 529 account. After all, there’s no loan you can use to fund your retirement.

3. Set up a Direct Deposit From Your Paycheck to Your 529 Plan.

Designating a percentage of your paycheck for automatic deposit to your 529 account can make saving a seamless, set-it and forget-it process.

4. Avoid Overfunding.

Withdrawals for non-qualified education expenses could incur a 10% penalty, as well as additional income tax on the earnings portion of the withdrawal. Options to avoid this penalty can include transferring funds to the beneficiary’s Roth IRA or using the funds for another family member’s education. Proper calculation and guided planning with a financial advisor over the course of the account’s lifespan can possibly prevent this situation.

5. Take Advantage of Gifting and Superfunding.

You can front-load your 529 plan through a combination of gifts from family and friends and your own lump-sum contributions to speed up the growth of your fund. Plus, those who give may qualify for a state income tax deduction for 529 plan contributions. This benefit, known as superfunding, means that your money has more time to compound interest.

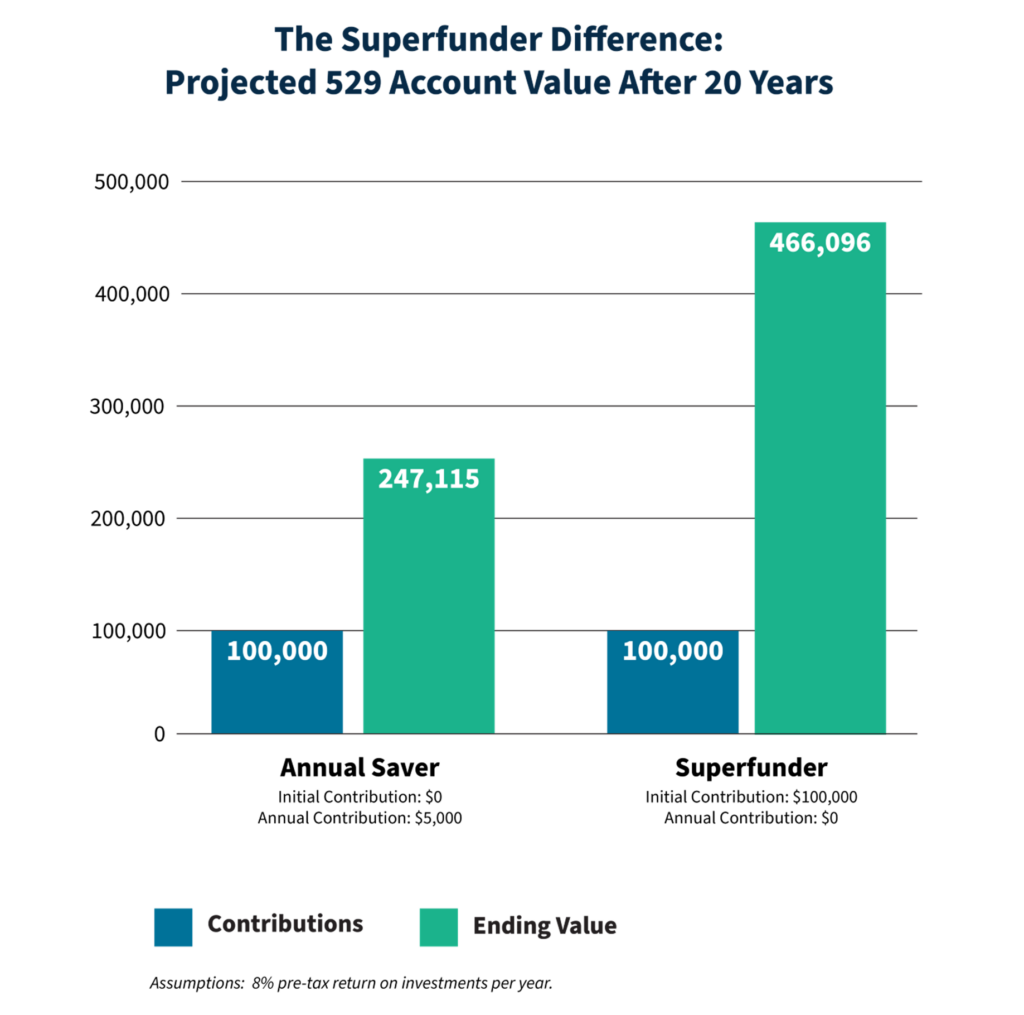

For example: Let’s look at two accounts that both contributed $100,000 in total over 20 years. Account 1, “Annual Saver,” diligently contributed $5,000 to their child’s 529 plan each year. Account 2, “Superfunder,” contributed a lump sum of $100,000 when their child was born, and never contributed again. As you can see below, both couples contributed the same, but the Superfunder account ended up with almost 50% more money in the 529 plan.

6. Adjust Portfolio Allocation as College Approaches.

As your beneficiary gets older, you can gradually shift your investments to reduce exposure to day-to-day market fluctuation, ensuring your funds are available when needed.

7. Enlist a Financial Advisor to Ensure You Maximize the Benefits and Achieve Your Goals.

While 529 plans offer many advantages, they have complex rules, risks, fees, and options that can make for a challenging investment process—and you don’t want to leave your child or loved one’s educational future up to chance. A financial advisor can assist you in plan selection, asset allocation, and long-term financial planning to make the most of your investment and ensure financial success.

How SC&H Can Help

At SC&H, we offer comprehensive, personalized, tax-focused financial solutions to help you achieve your goals and safeguard your family’s future. We design a customized college savings roadmap with a bigger picture in mind. Education savings are one part of a holistic approach that considers your goals and financial situation, ensuring all the pieces of your financial puzzle fit together. Want to learn more about our approach? Contact our team today and embark on your journey to financial success.

Advisory Services offered through SC&H Wealth the doing business as name (“DBA”) of SC&H Financial Advisors, Inc. SC&H also offers advisory services through the doing business as name of SC&H Core. SC&H Financial Advisors, Inc. is a wholly owned subsidiary of SC&H Group, Inc.

The information presented is the opinion of SC&H Wealth. and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance.