Authored By Ryan Frank | Principal, SC&H Financial Advisors, Inc.

We all want to pay less in taxes, as minimizing our tax liabilities allows more of our money to work for us. Tax-efficient investing can help achieve this. However, it requires that you strategically plan ahead. The five following investment strategies will help you minimize your tax burden and grow your net worth.

1. Consider Tax-Efficient Mutual Funds and ETFs

Everyone knows that certain accounts are tax-advantaged, but not everyone knows that certain investments can also be tax-efficient.

Investments with built-in tax efficiencies, such as exchange-traded funds (ETFs) and tax-efficient mutual funds, may help minimize your tax burden. When it comes to investing, it doesn’t matter what you make; it matters what you keep. If you give away half your money in taxes, you’ve reduced your profits regardless of your revenue.

ETFs and tax-efficient mutual funds are usually not as vulnerable to year-end capital gains. Their tax efficiency can reduce the amount you need to spend when you file your 1040.

2. Weigh Your Asset Location Distribution

Asset location minimizes taxes by dividing your assets among taxable and nontaxable accounts. A taxable account requires you to pay taxes on interest, dividends, and capital gains within the year they are earned. A nontaxable account, such as an IRA, allows you to defer taxes until the time in which you distribute money from the account.

Put investments that are not tax-efficient in accounts where you can defer taxes. Due to tax laws, not all types of investments are tax-efficient — such as bonds. Holding all taxable bonds in your retirement accounts is important because the interest income they earn each year is sheltered within the retirement account.

Likewise, hold tax-efficient investments, such as individual stocks and equity ETFs, in taxable accounts. When held in taxable accounts, the growth on these investments will be taxed at capital gains tax rates when sold, which for most is less than ordinary income tax rates when withdrawn from your retirement accounts.

3. Decide Whether to Pay Taxes Now or Later Depending on Income

In general, people are in a higher tax bracket while working than when retired. When you put money into 401Ks, 403Bs, and Traditional IRAs, you are allowed to defer a portion of your income and its corresponding growth into your retirement years, when you will most likely be in a lower tax bracket.

Conversely, if you plan to be in a higher tax bracket in retirement (e.g., you are expecting a significant increase in wealth, such as inheriting money from a relative or taking over your family business), you may look to take advantage of being in a lower tax bracket currently. If this applies to you, you should participate in these retirement plans but contribute to a Roth IRA option if available.

4. Look for Opportunities to Offset Gains

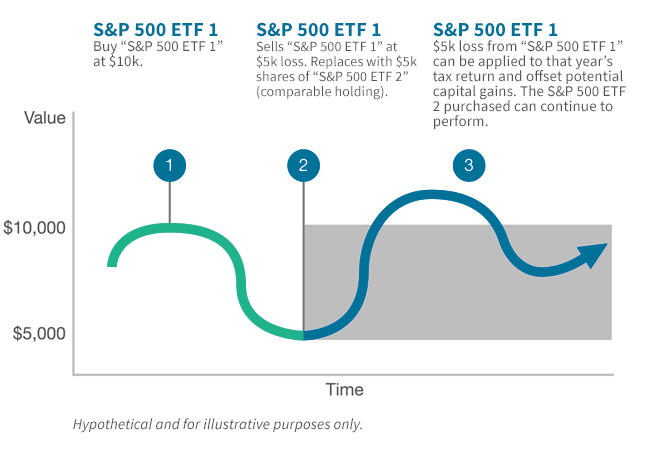

Fundamentally, you pay tax on the net amount of your capital gains. Look through your portfolio to find investments with an unrealized loss. By liquidating these positions, you can offset realized gains in that year and still maintain exposure to the investment sold by implementing a strategy called tax loss harvesting.

In years in which you have realized capital losses, you may use those losses to offset taxable capital gains that have also been realized. If there are losses left over, you may deduct up to $3,000 of net losses annually to offset ordinary income on your federal income taxes. You can also carry forward losses to future tax years.

Example of Tax Loss Harvesting

5. Make the Most of Your Charitable Giving

Instead of donating cash to your charity, church, or other philanthropic endeavors, you can gift appreciated securities such as mutual funds, stocks, and ETFs. There are also clever ways to donate securities within trusts to avoid harsh taxation. When you donate these securities, you do not pay any capital gains on the growth.

Imagine that you bought Amazon stock for $5,000, and it’s now worth $10,000. Selling this stock would net you $5,000 in profit, which would then be taxed as a capital gain. If you donated the same stock to charity, you wouldn’t need to pay capital gains. Instead, you’d avoid the tax, and further, you would get a charitable giving deduction as well (limited to 30% of your adjusted gross income).

Once you are age 72, you must begin withdrawing from your retirement accounts (required minimum distribution or RMD). Up to $100,000 of your RMD may be donated to a qualifying charity. This is called a qualified charitable distribution (QCD). Whatever you donate is not considered taxable income.

Plan Ahead to Avoid Headaches

The above five strategies require coordination between your investment advisor and tax accountant. Many times, your tax professional is not a licensed financial advisor and/or is not familiar with these investment strategies.

At SC&H, we provide these services under one roof. Working with both an experienced financial advisor and a CPA who understands how to invest can help you reduce your tax liability while also making sure you are investing properly for your goals. If you have a question about investing tax efficiently or would like to work with our team, please reach out today.

Advisory Services offered through SC&H Financial Advisors, Inc. SC&H also offers advisory services through the doing-business-as name of SC&H Core. SC&H Financial Advisors, Inc. is a wholly owned subsidiary of SC&H Group, Inc.

The information presented is the opinion of SC&H Financial Advisors, Inc. and does not reflect the view of any other person or entity. The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance.