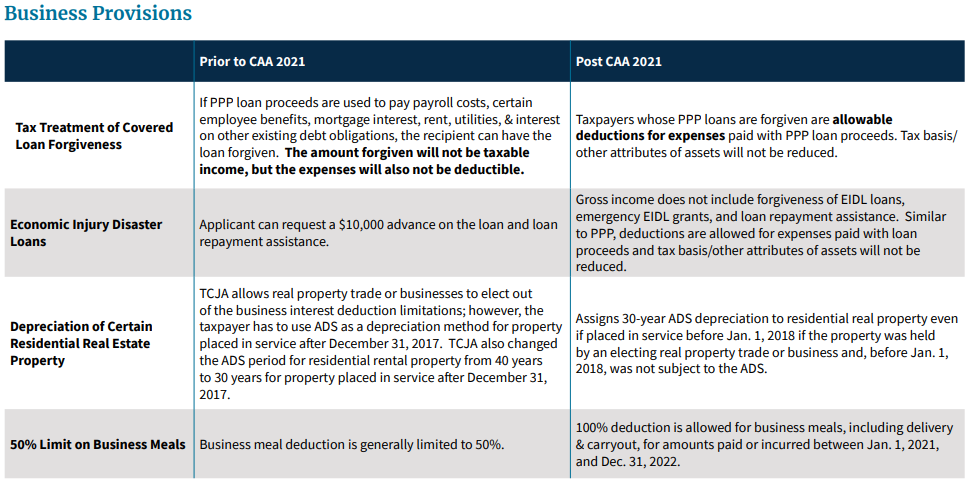

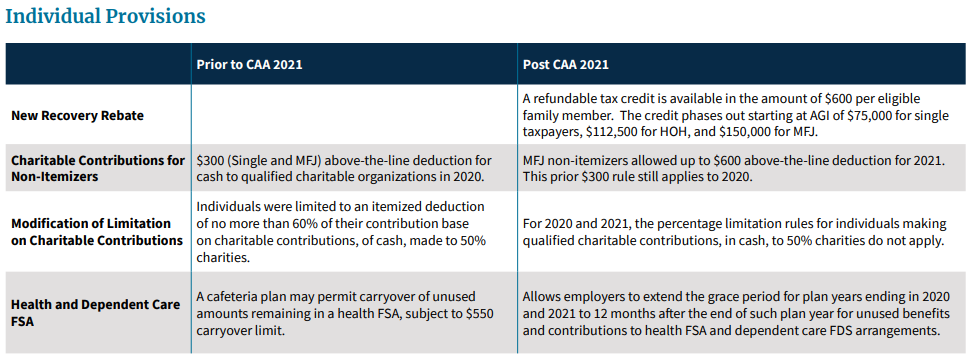

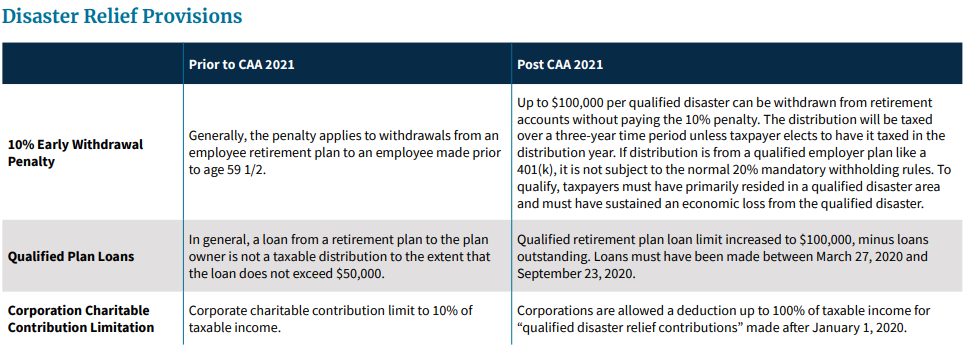

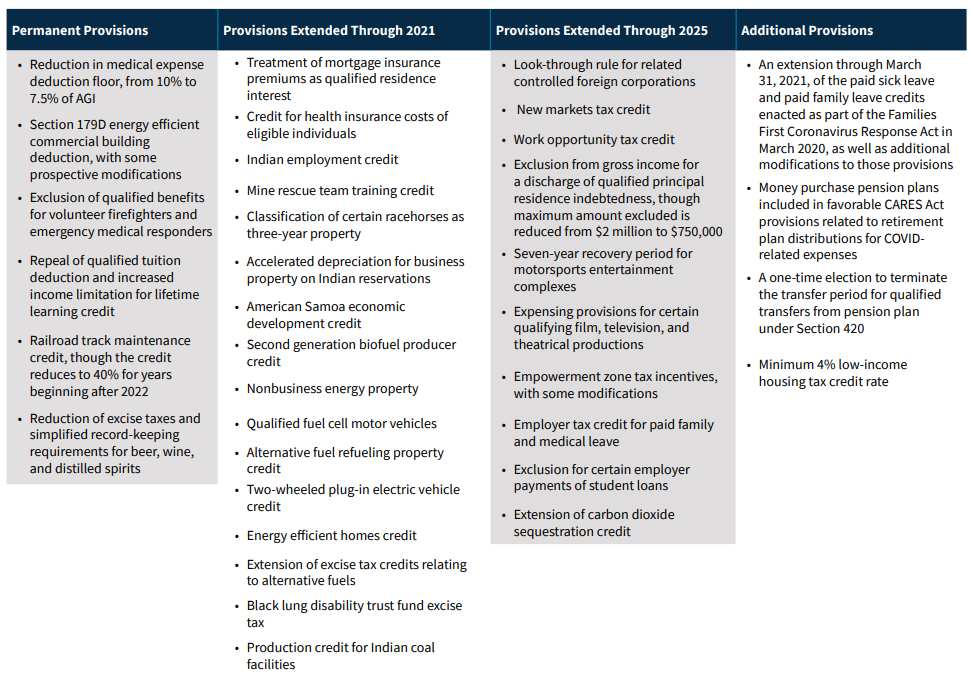

The COVID-related Tax Relief Act of 2020 (COVIDTRA) and the Taxpayer Certainty and Disaster Tax Relief Act of 2020 (TCDTR), both part of the Consolidated Appropriations Act, 2021 (CAA, 2021) contains numerous provisions related to businesses and individuals.

Here is a summary of some, not all, of the key components.

[sch_full_width_image]

[/sch_full_width_image]

[sch_related_resource]Want to Download the Full PDF? Click Here.[/sch_related_resource]

Related Insights

Blog

What is Microsoft Fabric? The AI-Powered Tool for Advanced Analytics

Blog | Case Study

Driving Growth: How a Trucking Company Increased its Revenue by 41%

Blog

Achieving Microsoft SSPA Compliance: A Supplier’s Guide to DPR v9 Updates

Blog

2023 Community Impact Report: Empowering Change Through Community Service

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.